Slides & Script

Build your webinar slide by slide with script narration

1

Slide 1: Introduction - The Current Rate Environment

Welcome everyone. Today, we're cutting through the noise to discuss where the 'good rates' actually are in this complex environment. We know central banks have been aggressive, leading to sustained high rates. This isn't just about expensive debt; it's about the significant disparity between what it costs to borrow and what you earn on cash. Our focus today is strategic allocation—how businesses can efficiently manage their liquidity and capital structure.

2

Slide 2: Securing Favorable Borrowing Rates (The Debt Side)

When looking for debt, the traditional bank loan isn't always the best option anymore. We're seeing a significant migration to private credit funds, which offer flexibility and speed, often beating traditional banks on terms for middle-market companies. Don't overlook strong relationships with regional banks, especially if your business is locally focused. For larger capital needs, structured finance, where specific assets back the loan, can dramatically lower the perceived risk and, consequently, the rate. Finally, active hedging is crucial to protect against future rate hikes.

3

Slide 3: Maximizing Returns on Cash (The Yield Side)

On the flip side, cash should not be sitting idle. The days of 0.1% returns are over. Money Market Funds and High-Yield Savings are the baseline for immediate liquidity. For slightly longer horizons, short-duration Treasury Bills are highly attractive due to their safety and federal tax treatment. Many businesses are implementing 'cash ladders,' staggering maturities of CDs or T-Bills to ensure ongoing liquidity while capturing higher yields on longer-term tranches. If you hold significant balances, always negotiate institutional deposit rates directly with your banking partners.

4

Slide 4: Alternative Funding and Efficiency

Beyond traditional debt and cash management, businesses are finding 'good rates' through efficiency. Supply chain finance, where you negotiate discounts for paying vendors early, often yields an implied return far exceeding what you could earn on liquid assets. Fintech platforms are filling gaps for specific, often smaller, financing needs. Most importantly, in a high-cost debt environment, internal efficiency—reducing the need for external capital through better inventory or receivables management—is the cheapest 'rate' of all. This environment forces a critical re-evaluation of the debt versus equity balance.

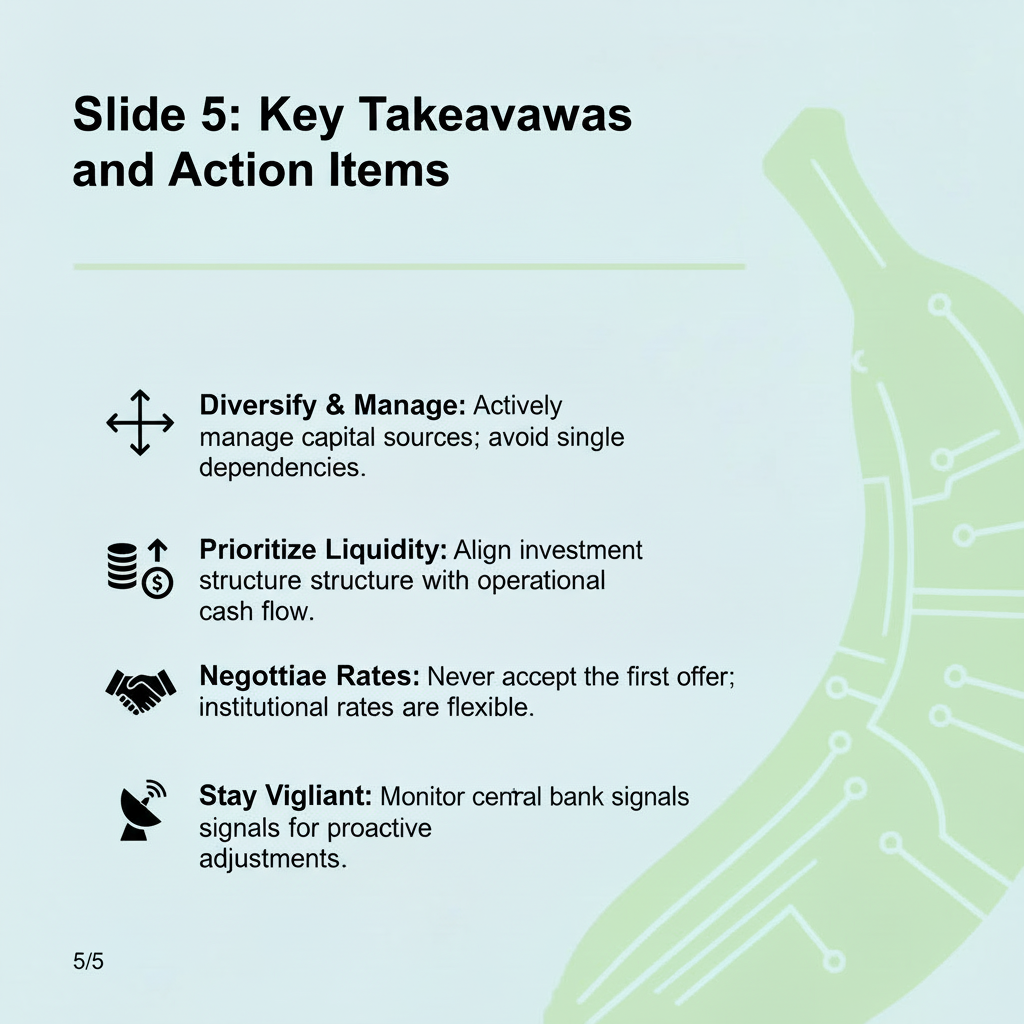

5

Slide 5: Key Takeaways and Action Items

To summarize, the 'good rates' are found through active management and diversification. Don't rely on a single source for capital or a single vehicle for cash. Prioritize liquidity—ensure your investment structure aligns with your operational cash flow. And finally, never accept the first rate offered. Institutional rates are negotiable. Stay vigilant regarding central bank signals, as proactive adjustments will be key to maintaining a competitive edge.